.png?width=11229&height=5299&name=Copy%20of%20LDA%20Logo%20RGB%20(1).png)

.png?width=590&height=590&name=Launched%20(3).png)

It has been 20 years since the formal push for the adoption of a needs-based sales approach began...

The Strategy: Shifting from "Account A" to "Account B"

Tax season is upon us and for many advisors across Canada that means it will be time to meet with your clients and revisit their tax strategies for their estates and/or businesses. While it is very common to use Life Insurance to bridge gaps in coverages, there are many ways, that when leveraged as an asset, life insurance can provide substantial benefits and allow clients to keep more of their money.

Think of your client’s net worth in two buckets.

- Account A: Their non-registered or corporate investment portfolio. It is exposed to annual taxes on interest, dividends, and capital gains.

- Account B: A permanent life insurance policy (Whole Life or Universal Life).

By reallocating a defined amount of capital from Account A to Account B, you aren't "spending" money; you are moving it to a tax-exempt environment. This shift maximizes the net estate value by eliminating the "double taxation" (tax on growth + tax at death) typically associated with traditional investments.

The Corporate Advantage: The CDA Lever

For business owners, the "Account B" strategy offers a unique corporate lever that is particularly relevant in today's fiscal climate. In our February look at 2026 trends, Henry Korenblum described leveraging the Capital Dividend Account (CDA) to extract capital from private companies as “The Holy Grail of Tax Planning.”

When a corporation owns the policy, the death benefit (minus the policy’s Adjusted Cost Basis) creates a significant credit to the CDA. This allows the corporation to pay out tax-free capital dividends to the estate or surviving shareholders. It is one of the few remaining ways to unlock "trapped" corporate surplus and move it into the hands of heirs without the standard 40%+ dividend tax hit.

Leveraging LDA for High-Impact Presentations

One of the biggest hurdles in this strategy is helping clients (and their CPAs) visualize the flow of money. This is where Life Design Analysis becomes an essential tool in your tech stack.

LDA allows you to:

- Compare Multiple Policies: Add multiple carrier illustrations to the same LDA report, allowing you to compare different payments or carriers

- Showcase Policy Growth: Move beyond static carrier illustrations. Use LDA’s dynamic charts to show how the "Cash Surrender Value" and "Total Death Benefit" stack up against a traditional taxable investment over 20, 30, or 40 years.

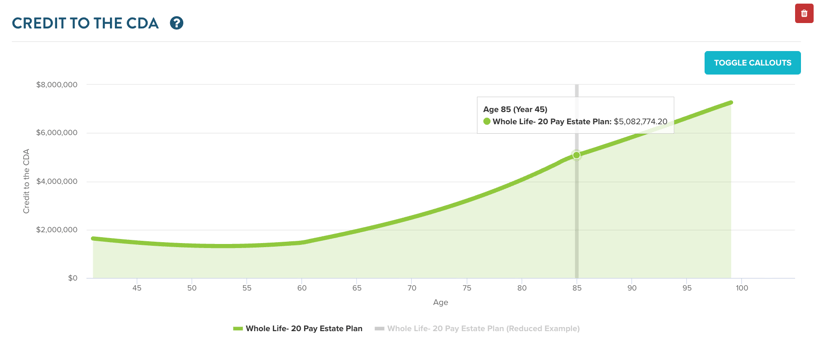

- Visualize the CDA Credit: LDA’s Corporate Estate Transfer reports specifically break down the projected CDA credit, showing the exact amount that can be distributed to heirs tax-free.

- Stress-Test Scenarios: Use the "Reduced Dividend" toggle to show how the strategy performs even if carrier dividend scales fluctuate. This builds immense trust with skeptical clients and analytical CPAs.

- Compare the IRRs: Automatically calculate the Internal Rate of Return (IRR) on the death benefit, proving that a life insurance policy can often outperform fixed-income portfolios on a risk-adjusted, after-tax basis.

2026 Tax Season: The Wealth Planning Lever

As we head into tax season, this strategy serves as a critical lever for your clients' current filings:

- Passive Income Mitigation: Under the current rules, corporate passive income over $50,000 grinds down the Small Business Deduction. Since growth inside a life insurance policy is not considered passive income for this test, shifting assets to Account B can help your clients keep more of their active business income taxed at the lower small business rate.

- Crystallizing CDA Balances: Before your corporate clients file their 2026 returns, check if they have existing CDA credits. If they do, they may be eligible to withdraw tax-free dividends before potential future capital losses erode that balance.

- Liquidity Planning: Use an LDA report to show how a client can "be their own banker." By using the policy as collateral for a bank loan (Immediate Financing Arrangement), they can fund their 2026 business expansion or investment opportunities while keeping their death benefit and CDA growth intact.

Conclusion: Reframing the Conversation

Success in 2026 isn't about selling a policy; it's about presenting a solution to a tax problem. By using Life Design Analysis to prove the numbers, you transform a complex tax concept into a clear, visual strategy that clients can act on before the filing deadline.